Explosive growth for GenAI – Not all tools are catching the tailwinds

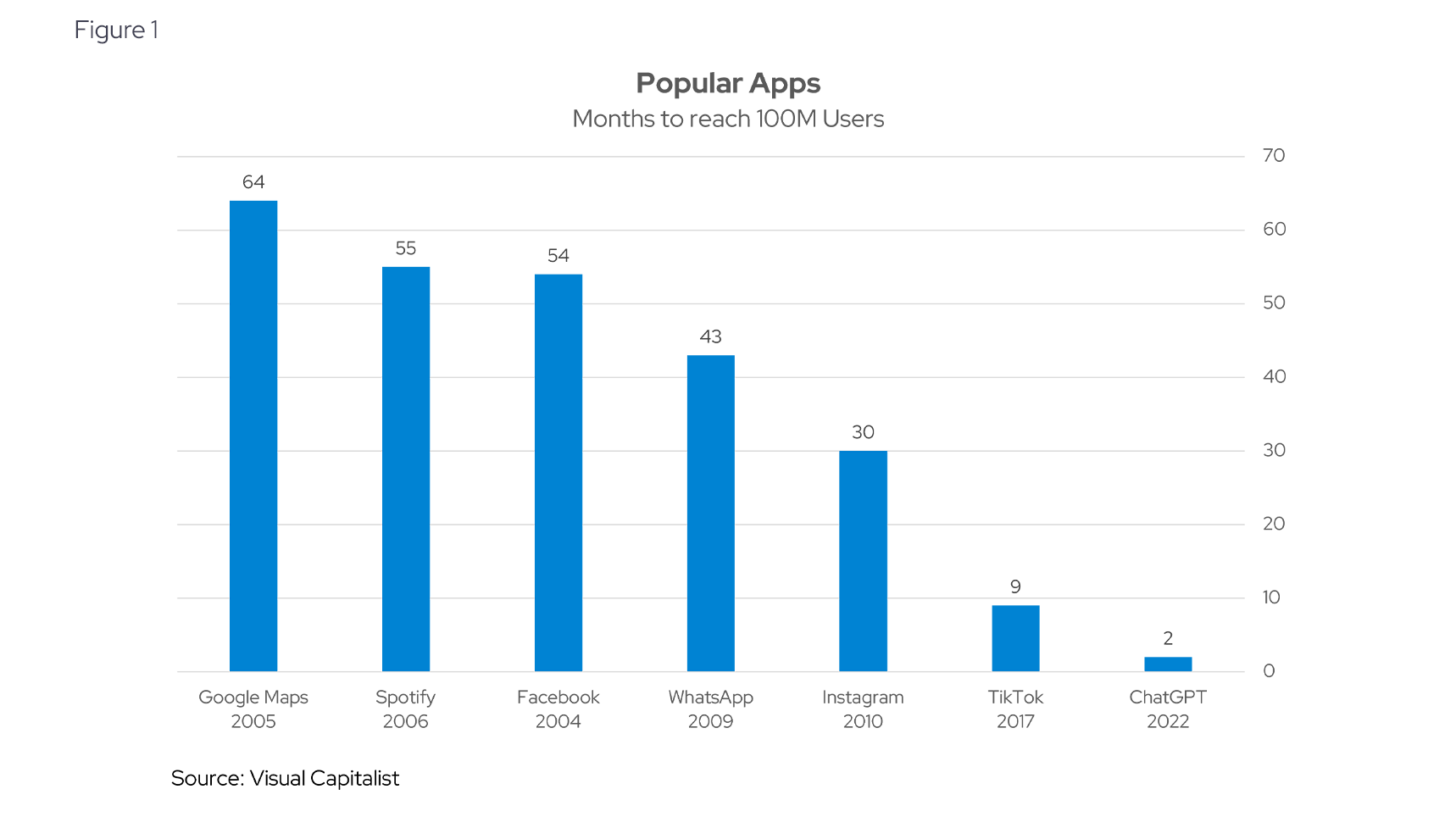

Generative artificial intelligence (GenAI), in particular models like OpenAI's ChatGPT, has quickly become a transformative force in the digital landscape, influencing consumer behavior and business operations alike. Recent reports highlight a dramatic increase in AI adoption. A recent McKinsey survey reports that AI implementation has more than doubled since 2017 and one-third of respondents said use GenAI regularly in at least one business function. Microsoft-backed OpenAI broke adoption records when it released ChatGPT on November 30th, 2022, and hit 100 million users in just two months. By some accounts, ChatGPT has over 200 million users today. As shown in Figure 1, this growth overshadows other popular apps’ adoption metrics like Instagram and WhatsApp. GenAI seems to be here to stay, as adoption grows across various industries.

As users embrace artificial intelligence, AI companies are spending vast sums of money on foundational model training (and the necessary capex associated) and are pivoting to monetization. Consumer spending on AI-driven products is on the rise, with IDC reporting that the AI software market will grow from $64 billion in 2022 to nearly $251 billion in 2027. Economic forecasts by PwC suggest that AI could contribute up to $15.7 trillion to the global economy by 2030, significantly impacting sectors like entertainment, retail, and customer service.

Where is GenAI making early inroads for consumers?

Investors are keen to ride the AI wave but given that the foundational model companies are largely private, investors haven’t had much purview into monetization trends beyond company data releases around funding rounds. To shed light into AI trends, we analyze consumer spending data from millions of accounts sourced from the deidentified Envestnet | Yodlee transactions database and explore trends in three key categories of GenAI: video & audio, text, and design & image. Models that do not fit into those categories represent a small portion of spending and were bucketed into “other”. Altogether, we reviewed 31 independent tools. Of these, several companies were chosen from each category for comparison, so the data shown below is not all-inclusive. It's worth a note that companies like Alphabet (GOOG) and Microsoft (MSFT) have invested in AI and have also developed their own in-house tools. In this article, we focus on the growth trends of independent tools and analyze their market share and positioning.

Rise of the chatbot: Consumer GenAI spending is dominated by text-based AI tools

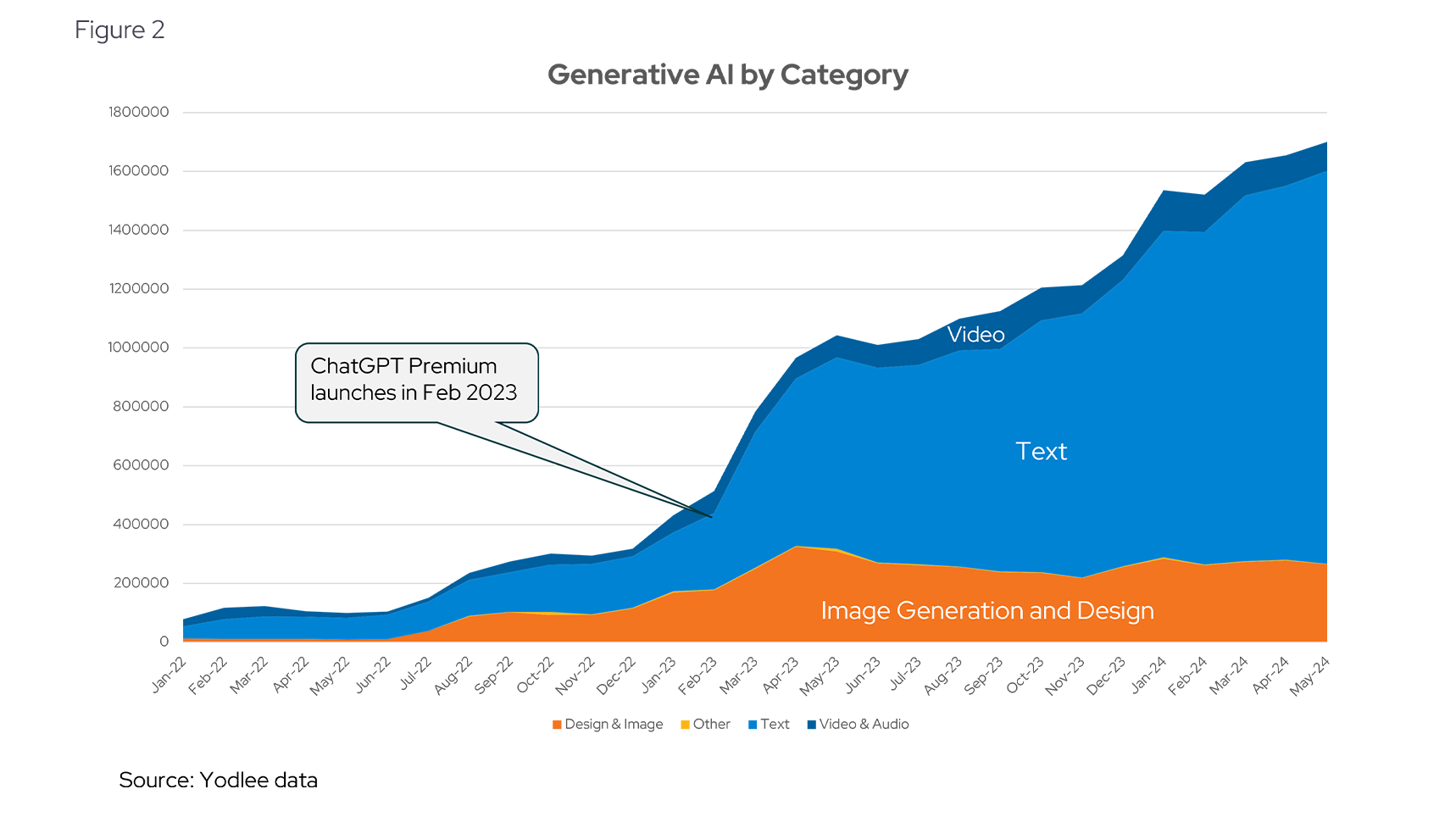

ChatGPT truly changed consumer adoption of GenAI tools and catapulted Large Language Models (LLM) into the mainstream. Looking at Figure 2, the text category appears to have seen the most significant growth in spending, especially from mid-2022 onwards. The rapid increase starting from early 2023, coincides with the release of ChatGPT in November 2022 and the launch of ChatGPT premium in February 2023. Having demonstrated product-market fit, these companies began to create monetizable product differentiation (free vs premium). The text category consistently maintains the highest spending and does not show signs of slowing, indicating widespread use and increasing demand.

While Chatbots are undisputedly the dominant force in GenAI spending, video & audio GenAI tools have also experienced notable growth, particularly from the second half of 2022. Design & image AI tools since appearing on the scene in early 2022, with notable growth starting around mid-2023 and leveling out since, as established incumbents began bundling GenAI functionality into existing design software packages (see Figure 2). ChatGPT now offers image generation via their Dall-e 3 model (included in premium) and will soon offer video generation.

Competition in GenAI is dog-eat-dog

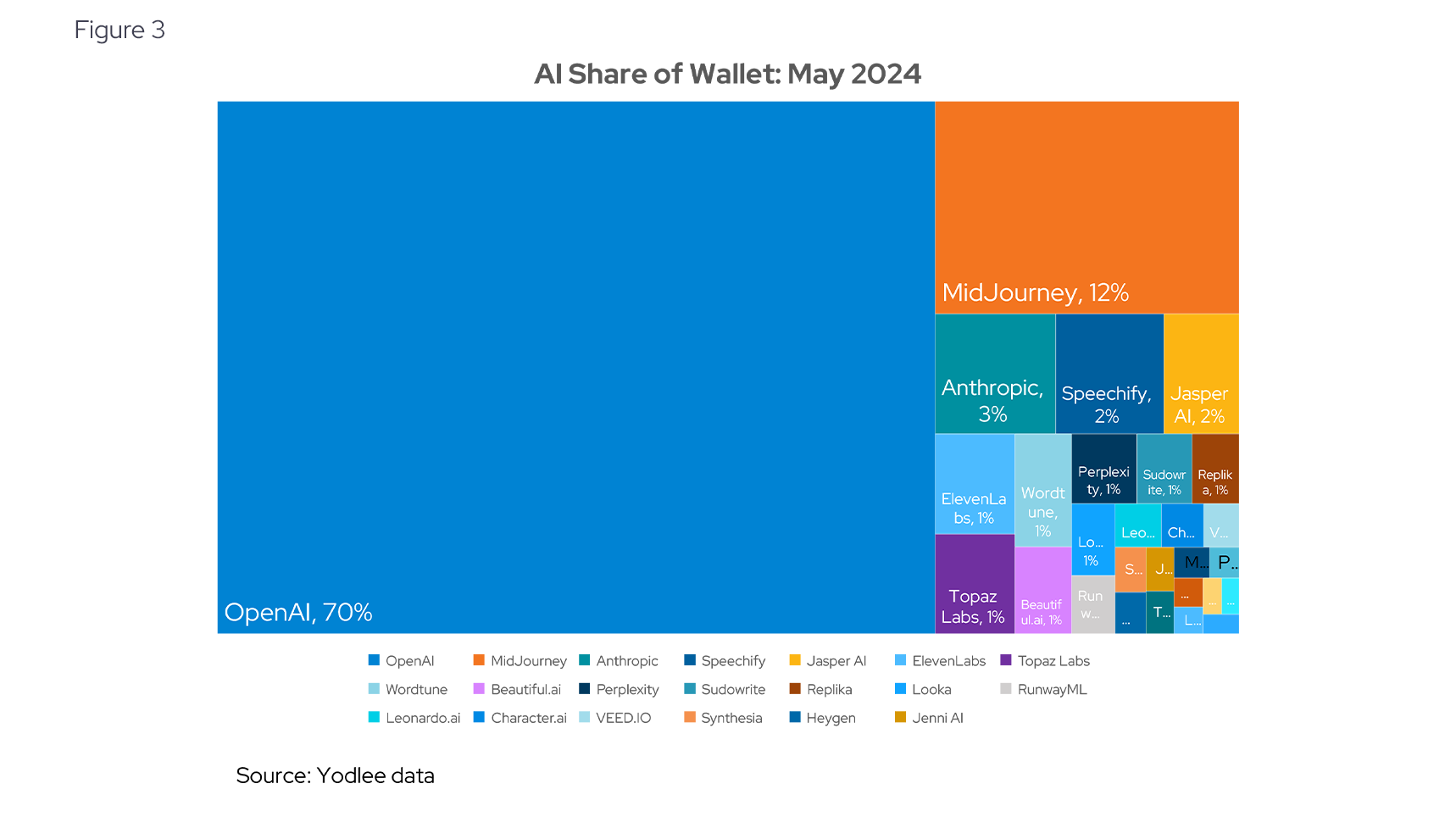

At the model level, OpenAI is the unsurprising winner with a 70% share of consumer wallet and no sign of slowing. Image generation app Midjourney accounts for 12%, and a close competitor to ChatGPT, Anthropic’s Claude takes 3% as of May. The other apps like Speechify (2%), and JasperAI (2%), trail far behind Open AI, according to Yodlee data (see Figure 3).

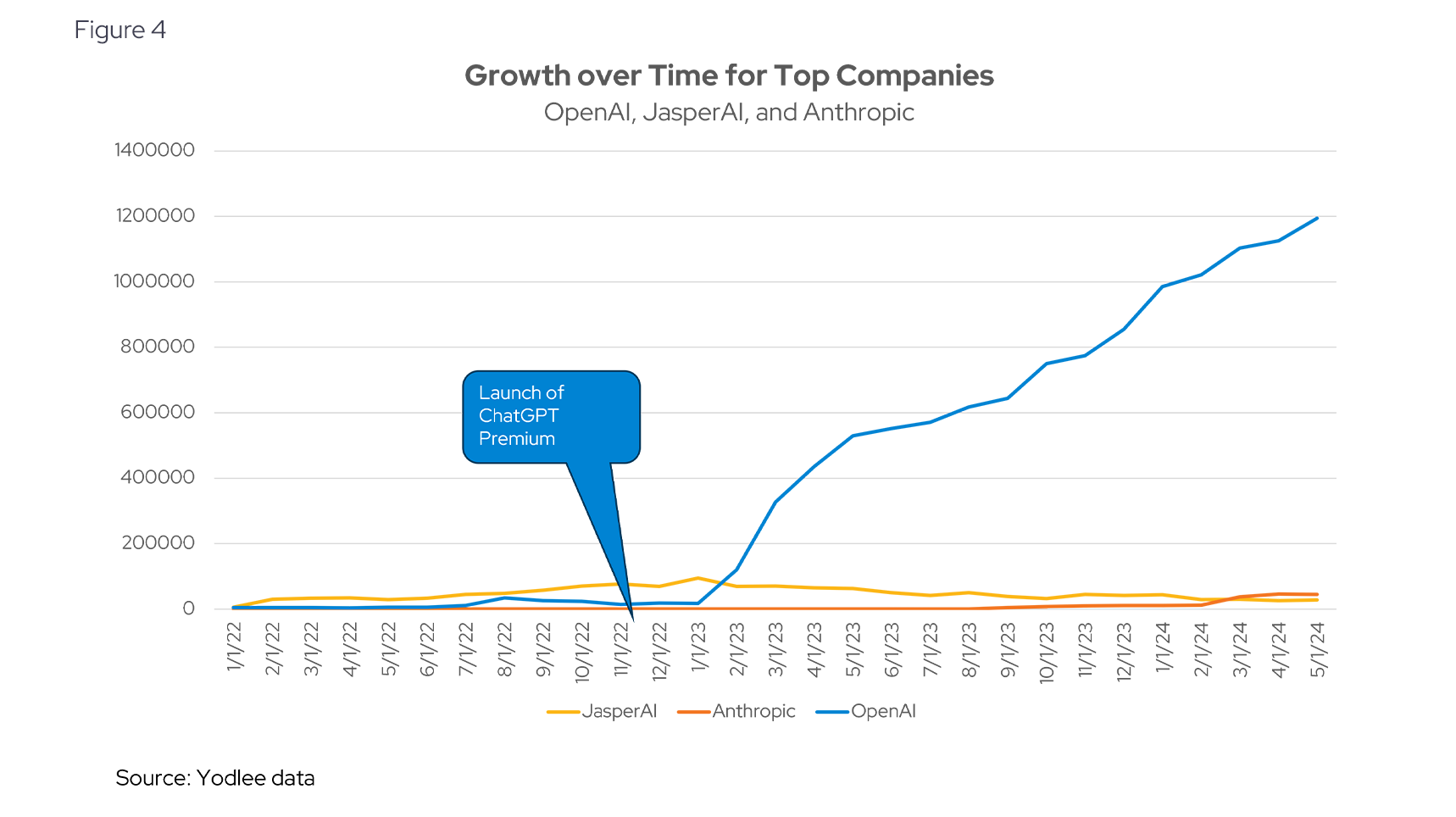

The launch of ChatGPT Plus in early 2023 marked a significant turning point, as illustrated by the sharp rise in consumer spending on OpenAI's ChatGPT immediately following its release (see Figure 4). Before the launch, both OpenAI and JasperAI had relatively low and comparable spending levels. Post-launch, ChatGPT experienced exponential growth with JasperAI’s declining to 2022 levels (see Figure 4). This shows that while Jasper did find a market fit, the emergence and growth of ChatGPT has likely taken a share of their revenues and continues to be a threat.

A later entry into the text-based AI tooling, Anthropic’s Claude was launched in March 2023 and seems to have seen reasonable growth beginning in March 2024 after the release of their Claude 3 model even though it is a close competitor to ChatGPT. While Anthropic is on the rise, the significant gap in spending between ChatGPT and the rest of the pack underscores Open AI’s dominance in the GenAI market.

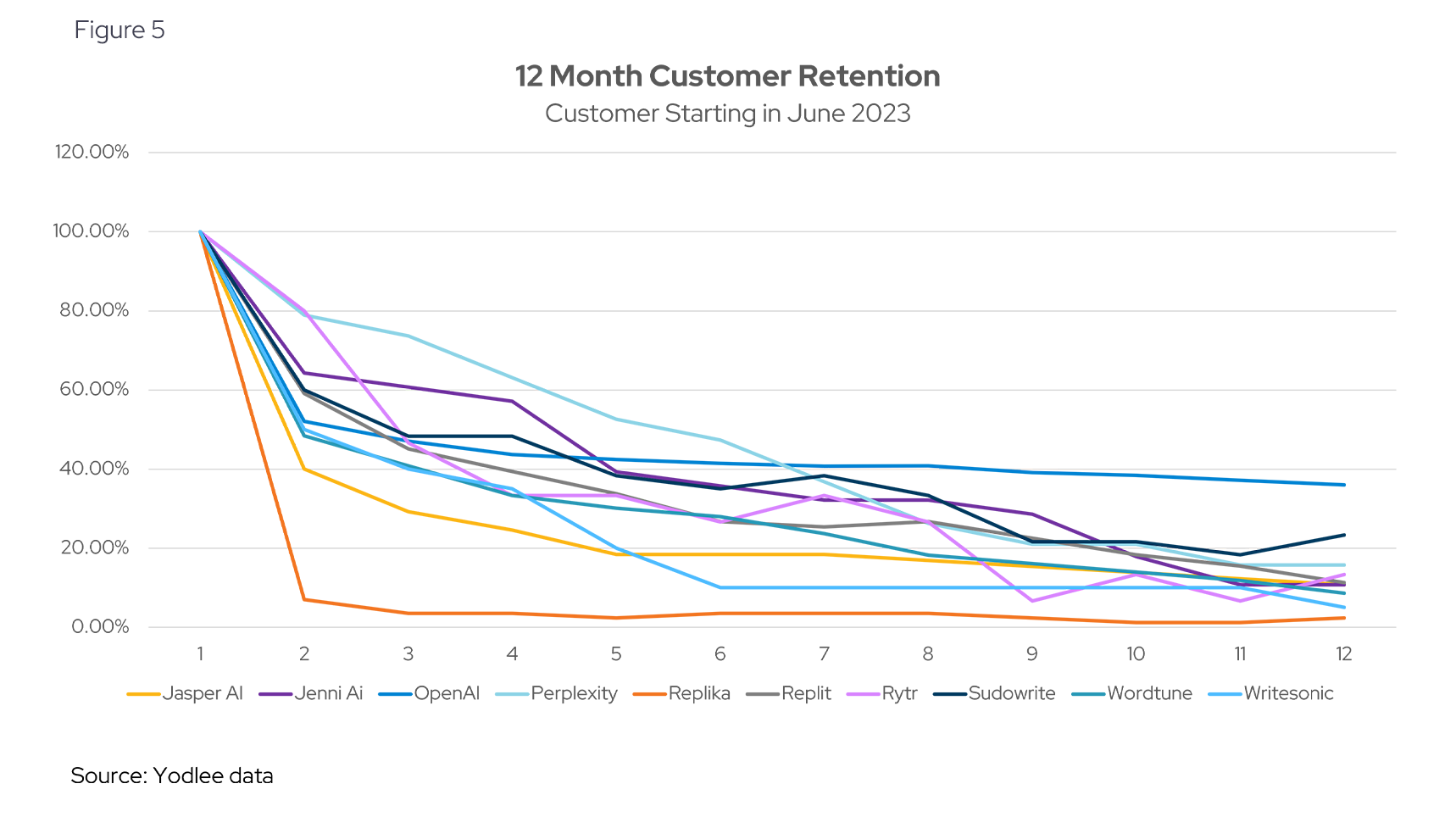

Customer retention confirms OpenAI’s dominance

In light of the competitive environment for text-based GenAI tools, customer retention over time is an important metric to track. It gives a sense that consumers are trying the paid versions to understand if there is value-add and quickly backtracking if the free versions are not delivering enough value. This underscores the durability of growth which will ultimately drive valuation normalization as hypergrowth wears off. Investors should keep monitoring this data across various apps to see which of them will be able to retain customers as this will be a key indicator of future revenue generation.

We used Yodlee’s data to look at user retention one year after adoption. We found that overall user retention has been challenging across the board indicating that customers try an AI app but often either discontinue using it or try a different app after a year (see Figure 5). OpenAI’s ChatGPT retains around 36% of users after one year, the highest value among AI apps. The AI-empowered search engine, Perplexity shows higher numbers in the first 6-months of usage but then trails off to just 13% of users 12 months into usage.

When compared with leading subscriber-based tech companies like Netflix, which has boasted a 2% month-over-month churn in Q1 2024, it’s clear that GenAI companies have some work to do on their value propositions when it comes to retaining paying customers. A caveat is that this is an early time for the industry and a lot of users are just trying out the technology to see if it works for them and retention may improve in the future especially as this technology is integrated into people’s workflow through other means.

The Evolution of GenAI and Metrics to Watch in This Dynamic Market

The growth of GenAI, particularly text-based tools like OpenAI's ChatGPT, has transformed the digital landscape. Despite the dominance of ChatGPT, other tools like Jasper AI, Quillbot, and Replika also show strong consumer engagement. Similarly, new entrants such as Anthropic and Perplexity are gaining traction, highlighting the highly competitive nature of the GenAI space.

With that said, retention rates will be a key metric for these companies, especially if going public is the long-term strategy. Therefore, moving away from daily/monthly active users and toward traditional metrics like lifetime value and customer acquisition cost as key indicators will illustrate persistent value added for returning customers. With that being said, it will be interesting to monitor these developments further and see if any competitors put up a legitimate challenge to OpenAI’s market share.

Want to see how transaction data can inform your investment process?

Learn more about Envestnet | Yodlee Merchant and Retail Insights and get a free demo from a sales representative.

About Envestnet Data & Analytics Income and Spending Trends

Envestnet Data & Analytics Income and Spending Trends utilize de-identified transaction data from a diverse and dynamic set of data from millions of accounts to identify patterns and context to inform spending and income trends. The trends reflect analysis and insights from the Envestnet | Yodlee data analysis team.